In the mid-2010s, seemingly a new of opportunity began to spread in crypto.

People gathered in conference halls, watched presentations, and bought into a vision of the future of money. A new cryptocurrency. Simple. Accessible. Profitable.

For millions of participants, the experience felt real.

Picture of a OneCoin event

There was just one problem:

The system they were investing in had no blockchain.

In this article we are going to open the casefile of OneCoin, reconstruct how the scheme operated and examine how one of the largest frauds in financial history was able to scale without any underlying technology.

Act 1 – The Vision

OneCoin was launched in 2014 by Ruja Ignatova, a Bulgarian entrepreneur with a background in finance and consulting.

Her message was simple: Bitcoin was complicated, slow, and already too late. OneCoin would be the next evolution. Faster. Easier. Accessible to everyone.

Ignatova speaking at one of Onecoins events.

Unlike Bitcoin, OneCoin was not presented as an open, decentralized network. Instead, it was sold through “education packages” that promised to teach users about cryptocurrency while granting them tokens that could be mined into OneCoins.

Participants were not just investors. They were encouraged to become promoters, earning commissions by recruiting new members into the system.

The structure combined elements of crypto, multi-level marketing, and financial speculation into a single product.

Within a few years, thousands of people across more than 170 countries had joined. Billions of dollars flowed into the system.

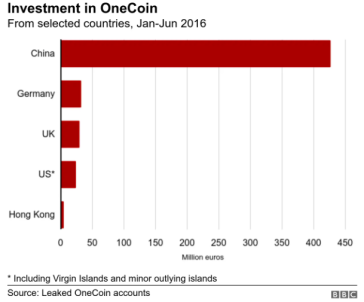

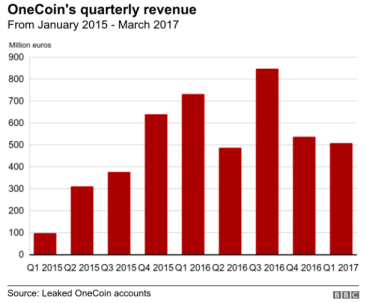

Two Charts depicting the investments and revenue of OneCoin. Source: Leaked Onecoin accounts/BBC

Act 2 – The Illusion

At its core, OneCoin claimed to operate on a private blockchain.

But unlike legitimate cryptocurrencies, there was no public ledger, no independent verification, and no open-source code. Transactions could not be inspected. Supply could not be audited. Mining was simulated through internal databases rather than actual computation.

The price of OneCoin was not determined by market but it was set internally.

Users logged into a centralized platform where balances increased and charts showed steady growth. To participants, it looked like a functioning cryptocurrency ecosystem. In reality, the system operated entirely off-chain.

What appeared to be technological infrastructure was a controlled database designed to simulate legitimacy.

Landingpage of Onecoin (currently not reachable) Imagesource: BBC

Act 3 – The Expansion

Growth was driven primarily through recruitment.

Members earned commissions for bringing in new participants, who in turn were incentivized to do the same. The more people joined, the more capital entered the system and the more convincing the illusion became. Large-scale events reinforced the narrative.

Ignatova appeared on stage in front of thousands, presenting OneCoin as a financial revolution. The branding, the language, and the scale all mirrored legitimate tech companies. For many participants, especially those unfamiliar with blockchain technology, the distinction between perception and reality became increasingly difficult to detect.

Warnings began to surface.

Regulators in multiple countries issued alerts. Analysts pointed out the absence of a verifiable blockchain. Critics described the structure as a pyramid scheme.

But the system continued to grow.

Act 4 – The Disappearance

In October 2017, Ruja Ignatova was scheduled to speak at a major OneCoin event in Lisbon.

But she never arrived.

Shortly before the event, she boarded a flight from Sofia to Athens and disappeared. She has not been publicly seen since.

Leadership of the operation passed to her brother, Konstantin Ignatov, who continued to promote the project until his arrest in 2019.

By this point, the structure had begun to collapse. Withdrawals were restricted. Internal markets froze. Investigations expanded across multiple jurisdictions.

Estimates suggest that more than 4 billion USD had been collected from participants worldwide.

FBI wanted poster of the notorious "Crypto Queen"

Act 5 – Conclusion

The OneCoin case demonstrated a fundamental property of financial systems:

Technology can create trust, but trust can also be manufactured without technology.

Unlike exploits such as The DAO, where vulnerabilities existed in code, OneCoin operated without any meaningful technical foundation at all. The risk was not embedded in software.

It was embedded in perception.

The absence of transparency, combined with strong narratives and aggressive distribution, allowed the system to scale far beyond what traditional fraud schemes had achieved.

OneCoin did not fail because of a bug.

It failed because it was never real to begin with.

This article continues the casefiles documenting major incidents in the history of cryptocurrency. Previous entries examined Mt. Gox, BTC-e, and The DAO hack, events that exposed failures in infrastructure and protocol design.

OneCoin revealed a different weakness.

The ability to simulate legitimacy at global scale.

If you found this casefile interesting, consider following the series as we continue tracing the history of crypto crime and collapse.

Stop the Dev.